Editor’s note: this is the first entry in our new column, Origin. Over here I explain why it’s so critical for Fresh Cup to address on a regular basis the issues, challenges, and, most importantly, the people where coffee is grown.

[T]here’s a quiet crisis in coffee, one that’s hard to discern because it’s taken a generation to unfurl and is experienced by the poorest, least enfranchised, least connected members of our industry. Making it worse, it’s a crisis that has benefited us on the buying side of coffee, making tackling this problem not just difficult but bad business, at least in the short term.

We’re not paying enough for coffee today, not enough to keep farmers planting coffee or laborers picking it. We’re not merely paying too little today, we’re paying way less than we ever have.

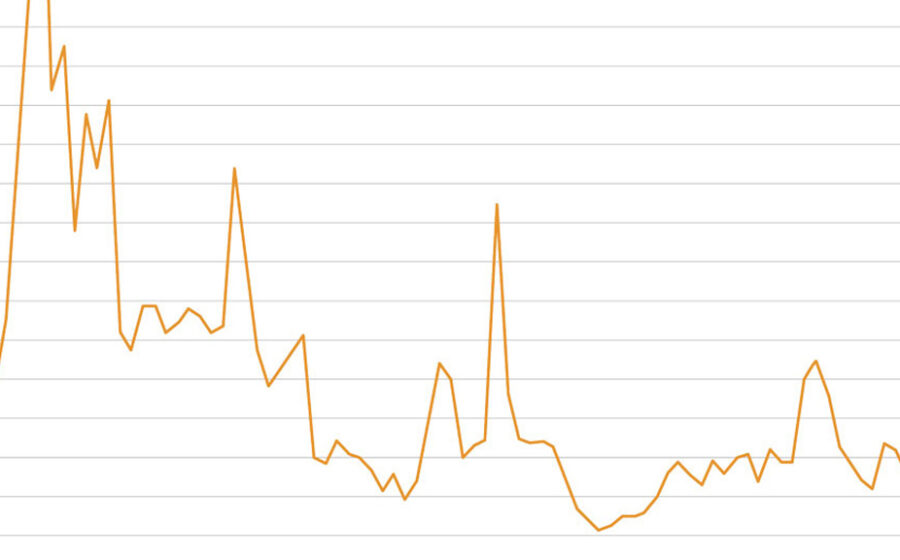

The data in the table above is a simplified graph of the C market prices (commodity coffee futures) since 1973 that plot approximate year-end and June prices. This is what you’d see if you looked at the historical price data available on investment sites. It shows the volatile reputation the C has earned, but also that the spikes don’t go much over $3 per pound of coffee and the lows have only gone below 50 cents once. On the day I’m writing this, the C is at $1.28, right at the historic median of about $1.20. It seems we’re paying about what we always have for coffee.

We’re not. Not even close.

In this graph, I’ve adjusted for inflation. Outside of a few spikes, it’s all downhill from 1980. The median price for this set is about $1.73. But even that doesn’t show how much less we’ve been paying for coffee. The median price from 1973 to 2000 is $2.93. For three decades, commodity coffee cost $3!

(The arbitrary January-June set means I left out the all-time high of $3.39 in April 1977, $13.32 today, and the April 2001 low of 42 cents, a catastrophic 56 cents today.)

This data does not connect one-to-one with the entirety of the coffee market. The C price isn’t what you will pay for a pound of green coffee on a given day—it’s the price for a futures contract, not a bag of coffee in a warehouse. It also doesn’t show us what farmers are paid. Premiums, grades, origin, regional differentials, co-op dues, transport, and plenty of other factors shift prices up and down on both ends of the chain. Still, it’s the marker of what green coffee has cost over the past four decades, even for the specialty side of the industry.

As much as our nook of the industry dislikes it, the C is the peg that all coffee prices hang on. Some certifications offer price floors (Fair Trade International guarantees a minimum of $1.40, for example), but their premiums are tied to the C. Some direct-trade importers and roasters have, to greater or lesser degrees, managed to detach themselves from the C price, and auctions are a true market outside of commodity, but direct-trade and auctions account for a sliver of coffee. And every story of a $30 auction coffee will compare it to the C price that day, because that is still the metric of coffee’s true cost.

The C price is the best gauge for what our industry pays the folks who grow our coffee, and we have been paying them less and less every year.

While we’ve done that, we’ve piled demands onto farmers. As their payouts splattered on the sidewalk, consuming countries asked for more certifications, increased transparency, improved growing practices, and novel processing methods. None of those are bad (I dig a red honey coffee) and those demands come with promises of premiums, but when a farmer goes through all that and looks at the $3 price paid by the roaster (which is probably not even the price she got) she’s surely glad to get a price better than the C, but she’s also thinking this is half the price her dad got in the eighties when all he had to do was drop it at the co-op.

That’s untenable.

In many origin countries, there is a strong belief that we have lost a generation of coffee farmers. I say it’s a belief because the data isn’t great (yearly numbers on farmer age is not what poor countries spend money collecting). But the average age of a Colombian coffee farmer is 55, and it’s the rare, usually wealthy, farmer who wants his child to inherit the business, so it’s a belief I share. I believe we’re losing the next generation, too.

Prices aren’t the whole story here, but talent follows cash, and if you can get paid more to farm another crop or to work an entirely different job, you won’t grow coffee. That goes doubly for laborers. Across Central America, most acutely in Guatemala, a major reason farms haven’t rebounded after roya isn’t just the cost of replanting: the labor force withered away too, either leaving the country or finding better pay.

A last point, one this data set does not prove but I believe correlates: the eruption of specialty coffee culture and the spread of small roasters in the mid-2000s is when coffee was at its absolute cheapest. I expect specialty coffee would have taken off even if prices were higher, but it’s worth considering what sort of springboard effect historically low prices had on the ability of roasters to enter the market and on the willingness of producers to cater to the desires of quality-focused buyers.

If this correlation is causal, then the industry as we know it owes its existence to the low price of coffee and the low income of farmers and workers. If we want our industry to continue, if we want to keep getting the amazing and ever-better coffees we love, we will have to find a way to balance that ledger.

—Cory Eldridge is Fresh Cup’s editor.

Data: tradingeconomics.com/commodity/coffee