In 2001, coffee’s commodity price crashed. Slow demand growth, coupled with booming production, drove prices to record lows. Between 1997 and 2001, green prices fell by 70%, to below 50 cents per pound. The ensuing crisis immiserated farmers and caused many to abandon coffee altogether.

After intergovernmental reforms failed to materialize, the coffee industry embraced a market-driven approach. Certifications like Fairtrade proliferated and grew in stature, while big brands introduced their own sustainability programs.

It was the coffee industry’s embrace of these voluntary, market-based standards that inspired the creation of the first Coffee Barometer, published in 2006 by a group of Dutch NGOs. The inaugural report was short, focused on just the five largest roasters in the Netherlands, and featured a simple infographic that represented the amount of supposedly sustainable coffee each one had bought. “You started to see, okay, this is the projection of companies and what they are claiming versus the reality of what they are doing in practice,” says Sjoerd Panhuysen, lead author of the Barometer.

Over the intervening two decades, Panhuysen and his co-authors have published a new Barometer about every three years. During this time, they have examined the economic and social realities of the coffee industry, and tracked the sustainability pledges of some of the world’s largest coffee traders and roasters. The latest report, published last week, reflects on the progress made over the past 20 years.

Crucially, it asks the question: Is the industry any better off than when the Barometer began tracking it 20 years ago?

‘Meandering Through Time’

With each iteration since its first 2006 report, the scope of the Barometer grew. Later editions expanded focus beyond a handful of companies doing business in the Netherlands to the largest global coffee companies. Panhuysen’s team also started structuring each report around a different, topical subject.

In 2014, for example, the Barometer examined the impact of climate change on coffee farmers. In 2018, it was the consequences of corporate consolidation. “It feels like you’re telling the same story over and over again,” Panhuysen says. “To keep it interesting, you have to find ways of looking at the same subject matter in a different way.”

Rather than a specific focus this year, Panhuysen describes the 2026 Barometer as “meandering through time.” He says his team wanted to explore how the conversation around coffee’s biggest issues has changed over the past two decades—and, more pertinently, how the various solutions proffered by the industry have largely failed to solve its biggest problems.

After the price crisis of the early 2000s, Panhuysen says, the industry first embraced third-party certifications as the fix. Once that approach failed to solve coffee’s root problems, multi-stakeholder initiatives became more popular. Then the solution became providing a living income for coffee farmers, who often fail to even recoup their costs of production. “There is this immense belief that if we crack the living income issue, that we will solve most of the problems in the coffee sector,” he says. “But we also have to figure out how we are going to do it. I haven’t seen anyone putting up their hand, like, ‘Let me pay for it.’”

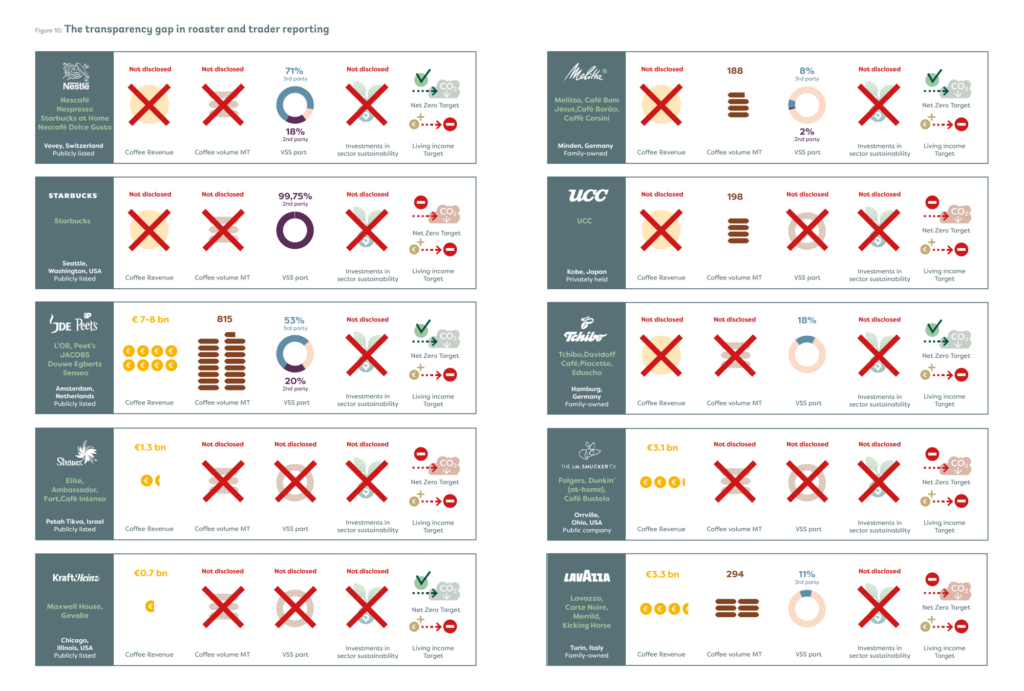

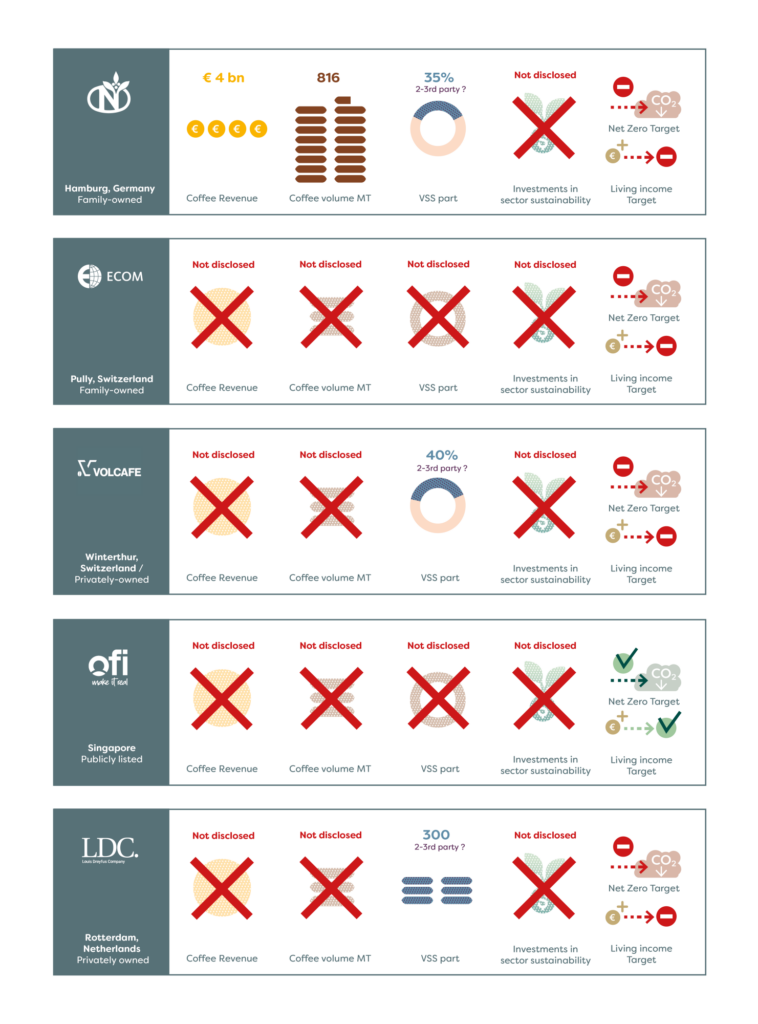

Even now, it’s still difficult to know exactly how much coffee the largest brands are buying, what they are paying, and how much is truly sustainably grown. Panhuysen and his co-author Frederik de Vries asked 15 of the biggest coffee companies for information about their sourcing, living income targets, and sustainability investments. The results are illustrated in a revealing infographic that shows a stark lack of transparency.

“Despite the talk in the sector of sustainability as a pre-competitive field, I think it’s completely the opposite,” Panhuysen says. “It’s a highly competitive field, and that’s why nobody is sharing any of this very basic information.”

Ambitious Goals, Mixed Results

In tracking how the coffee industry has progressed since 2006, the 2026 Coffee Barometer lays bare just how ineffective the industry’s market-driven solutions have been in solving its most glaring issues.

On the topic of certifications, Panhuysen and de Vries call the results “mixed.” The idea that consumers would pay more for certified coffees, and that those premiums would return to the farmers, didn’t happen at the scale needed. Many large companies have since introduced their own in-house sustainability programs, the authors write, which they see as “more efficient, adaptable, and easier to control than third-party alternatives.” Starbucks, for example, reports that 99.75% of its coffee is ethically sourced—via its own C.A.F.E. Practices program.

Multi-stakeholder initiatives (MSIs) were similarly ambitious, and have had similarly varied outcomes. Large companies and NGOs set up pre-competitive, collaborative platforms such as the Global Coffee Platform and the Sustainable Coffee Challenge in the mid-2010s. These MSIs were “designed to move beyond individual company action towards collective coordination, shared accountability, and structural change,” Panhuysen and de Vries write.

However, while there have been positives in the form of coordination among big players and subsequent scaling of sustainability impacts, the limits of this approach have also become clear. “The structural challenges MSIs were meant to address—notably unequal value distribution and chronic under-investment in climate resilience—remain largely intact after years of intensive collaboration,” the authors write.

Another focus of this year’s Barometer is the industry’s response to regulation. The European Union—the world’s largest coffee market—has a number of new directives due to come into force over the next few years. They include the controversial deforestation legislation known as the EUDR, which has been praised by environmental organizations but also criticized by industry groups for its possible impact on smallholders. There’s also the Corporate Sustainability Due Diligence Directive (CSDDD) which requires large companies to identify and address human rights and environmental issues within their supply chains.

Panhuysen sees this as a full-circle moment. “Our analysis in the coffee sector, 20 years ago, was that because of a lack of regulation, we need voluntary standards, and as a sector we can solve most issues voluntarily,” he says. “But that clearly has not really worked, so now it feels like we’re back to mandatory legislation.”

The new laws—there are also incoming regulations around forced labor and greenwashing—should help to guide the coffee industry in a positive direction, Panhuysen says. “However, we’ve also learned from the voluntary standards that companies tend to push most of the cost down to the farm level, and that’s probably going to happen again.”

‘Genuine Yet Insufficient’ Progress

The latest Coffee Barometer doesn’t pull any punches in its conclusions. “Over two decades, the coffee sector has repeatedly treated structural problems as technical fixes, and market failures as issues to be solved at farm level,” Panhuysen and de Vries write. They call the progress made during this time “genuine yet insufficient.”

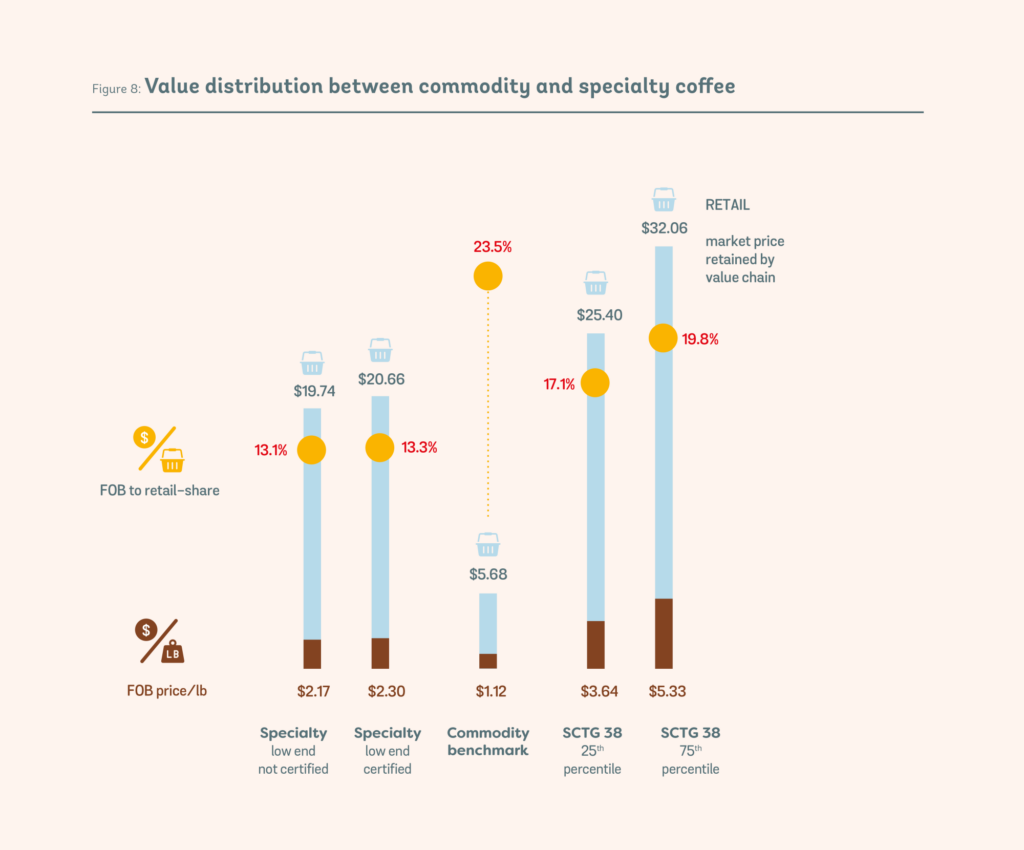

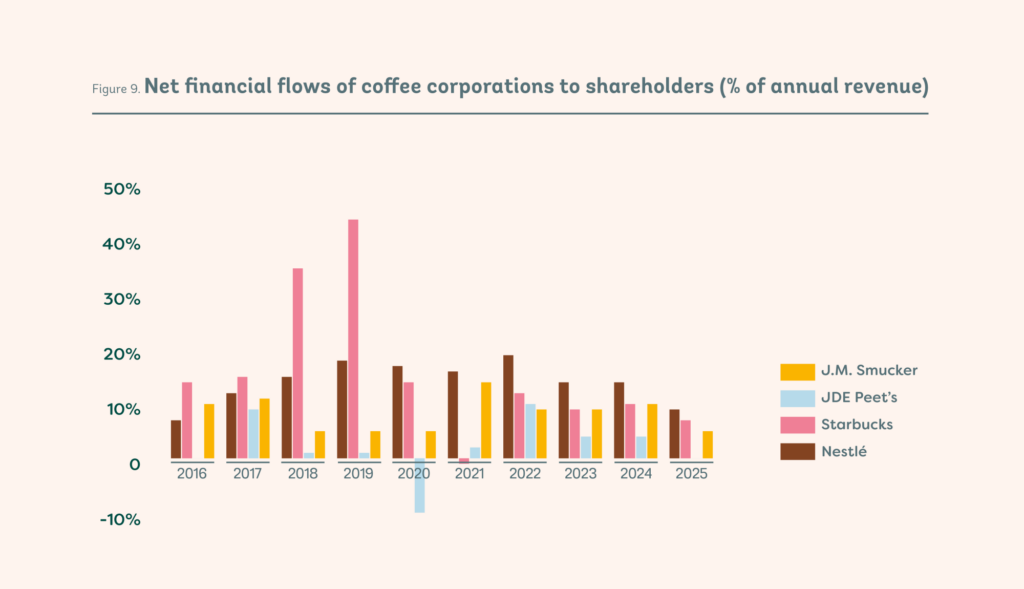

Despite a rise in commodity prices over the past few years, many smallholder farmers still live in poverty. Unpaid family labor continues to subsidize the wider industry, while much of the value created by the sector is extracted by its largest brands and their executives. The climate crisis is already impacting production around the world, yet many companies still lack a clear strategy to respond.

Meanwhile, much of the industry’s progress has been funneled through in-house sustainability programs and multi-stakeholder initiatives, which allow companies to control outcomes and leave little room for transparency or accountability. While in the near future regulation may offer a more enforceable set of solutions, Panhuysen notes that it will only work if the industry as a whole commits, and doesn’t just pass the costs down to farmers.

“Mandatory legislation is going to put more and more pressure on the sector,” he says. “But of course, the sector is built on an extractive model, so there are so many elements that need to be adjusted to get it right.”

The Barometer ends with a call to action, of a sort. The industry, Panhuysen and de Vries write, has a decision to make: continue with the status quo or commit to real, structural change. “The choice is not between sustainability and profitability,” they write. “It is between a model of sustainability that manages the appearance of progress and one that accepts the redistribution of value that a resilient coffee future requires.”