We’ve all heard actors across the coffee supply chain call for people to pay more for coffee in response to the low wages paid to farmers. Many farmers do not make enough to cover the cost required to produce coffee, meaning they’re growing coffee at a loss.

But would paying more for coffee on the consumer’s end actually result in more money for farmers? That’s one of the questions a new study, “The Grounds for Sharing: A study of value distribution in the coffee industry,” out Tuesday, June 18th, looks to answer.

“The issue of economic viability is constantly discussed in the coffee sector, specifically focusing on producers,” said Andrea Olivar, the strategy and quality director for Latin America at Solidaridad Network.

Through the Solidaridad Network, Olivar was part of a group, along with the Sustainable Trade Initiative (IDH) and the Global Coffee Platform (GCP), to commission a study “to estimate the distribution of value, costs, taxes, and net profit margins along coffee value chains, from coffee farmers to end-consumers,” according to the report.

Olivar said the report, which is 74 pages long, attempts to answer “if there was really enough value in the supply chain to make a profit and for farmers to have an income that is economically viable.”

“We wanted to have an objective view rather than assuming because this is what the coffee sector has been doing for a long time,” said Olivar.

The study, which took 18 months to complete, looks at the German coffee consumption market and four coffee-producing countries (Brazil, Colombia, Ethiopia, and Vietnam) to understand how value is distributed as coffee moves from producer to importer to roaster to retailer.

The three groups launched the report’s release in a global webinar on Tuesday, but for those who missed it, here are the key findings:

One: There is enough value in the coffee industry, but that value is consolidated at the consumption end

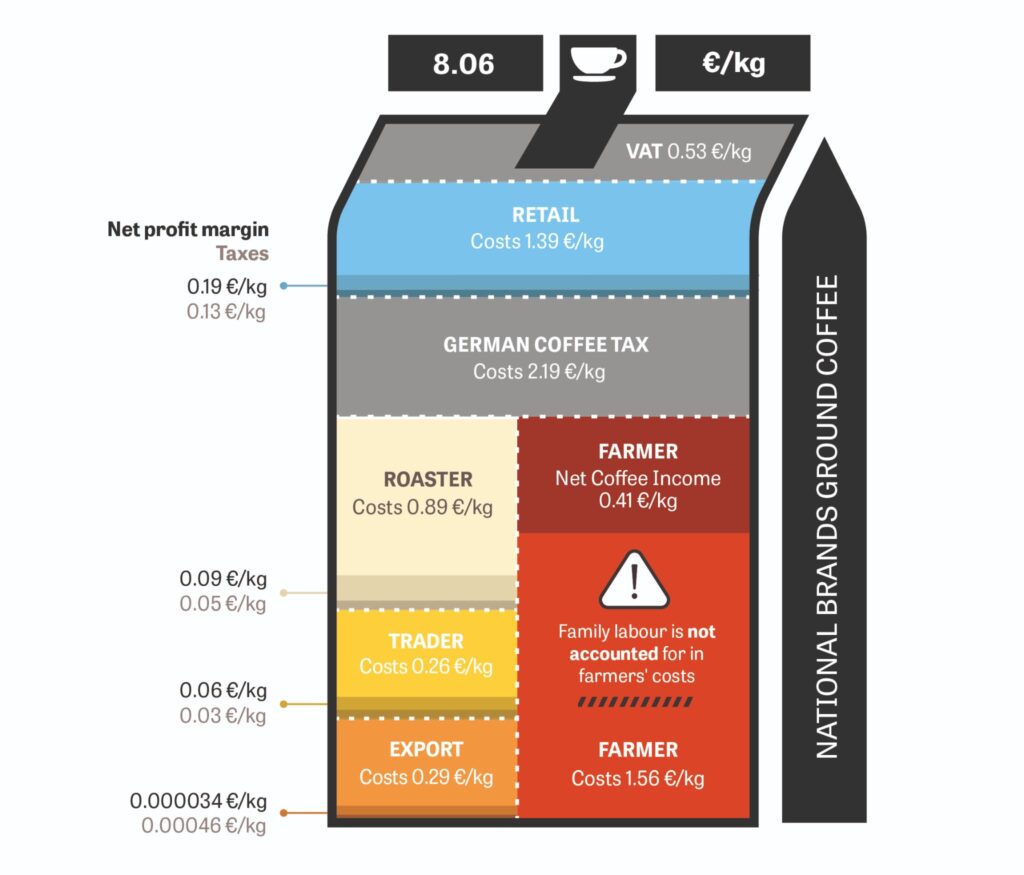

One of the main objectives of this report was to break down how value is distributed when looking at a kilogram of coffee. The report, which used “publicly available data from the German coffee market,” according to a press release, breaks down the value of a kilogram of coffee by percentage:

Around 20% of the value of coffee, across all formats, remains with producers, based on farmgate prices (or the actual amount a farmer is paid versus freight on board, or FOB, which is the price a buyer pays to an exporter and can account for other costs associated with transport).

This percentage seems higher than previously suggested estimates (a common estimate is around 10%), but that doesn’t mean farmers are making more than previously thought. “We have determined that some producers are making a profit, but the majority are not,” said Olivar. “Basically, they are contributing to the supply chain without making a profit margin.”

Roasters and retailers account for 21% and 22% of coffee’s value, respectively, while the other ~35% is distributed among taxes (nearly 30%), exporting, and transport costs.

“The study highlights that there is an overall profit to be made on all aggregate coffee products for the German market,” the report reads. “What is very clear for each of those, however, is that the added value concentrates in the downward part of the chain (from importer to retailer) and is limited at the farmer level.” Basically, there’s money in coffee — it just stays at the consumption end of the chain.

Two: We’re undervaluing family labor

The study also breaks down the value each supply chain sector takes relative to its profit. For every kilogram of coffee, farmers net an average of €.41 (44 cents USD). But that number is likely not as straightforward as it seems.

One huge hurdle the study identified is family labor: many smallholder farms operate with the help of family members, and that labor is hardly ever accounted for when discussing income — spouses, children, and siblings might be working on a farm, and the report identified that this labor often goes unpaid.

“If this is your income and you deduct the cost [to produce coffee], then the net income seems quite positive, but you’re not including the main cost,” Olivar said, which is family labor.

Three: When we increase value on the consumption end, that value does not trickle down to farmers

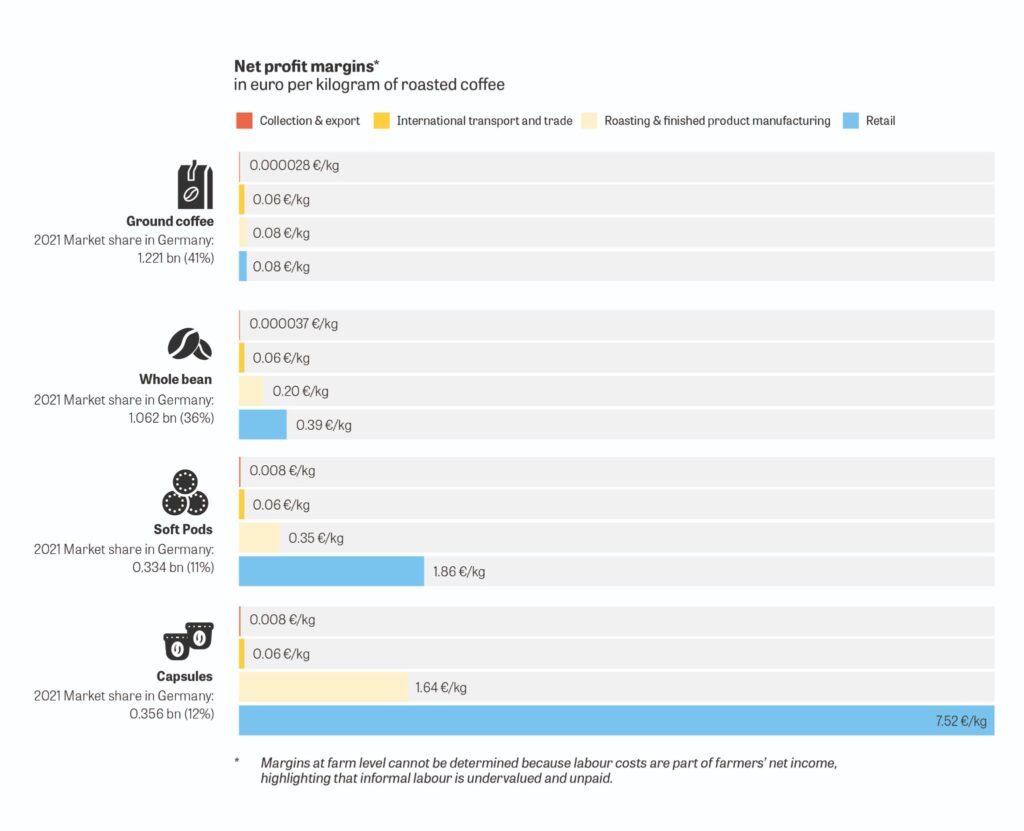

The report looked at coffee broadly but also broke down value distribution by certain types of coffee, like ground versus whole bean versus coffees with specific certifications. Perhaps the most significant differences in value distribution appeared in the coffee capsule sector.

Although capsules account for a small percentage of the coffee consumption sector in Germany, retailers stand to make a significant profit from them. Where retailers might be making a few cents per kilogram of coffee sold in whole bean or ground coffee, they make an average of €7.52 in profit per kilogram sold as capsules.

That value creation, however, isn’t flowing from retailer to producer. “A producer will hardly ever profit from that differentiation of that value in the market,” said Olivar.

“Estimates on capsules underline that there is an asymmetry between the high share of value accruing to the Retail and Roasting stages compared to the low share of value accruing to the Coffee cultivation stage,” the report states.

“I think that’s a key finding: that it doesn’t matter which product you’re selling in the end as a producer — I’m not going to be paid more if you’re selling capsules or if you’re selling ground coffee,” said Olivar. “If we ask today for consumers to pay more, there’s not a mechanism for that trickle down to producers.”

The study suggests that the value generated in the consumer-facing end of the supply chain stays with retailers, which calls into question the premise that compelling consumers to pay more for coffee will translate to higher wages for farmers.

Four: Risk and value look different for actors across the supply chain

Olivar also notes that it’s important to contextualize value and profit. For many retailers, coffee beans are not the only things they sell, but for producers, coffee is often the only crop they grow. “[The ability to manage risk is essential for value. If you are a producer, you don’t have that option to manage your risk like other actors in the supply chain.”

“The ability to make margins is enabled through the ability to diversify a portfolio across products and countries,” the report reads. “However, these tools are also not equally accessible across the supply chain. Upstream, there is often less opportunity to diversify.”

Five: Interventions have to be direct

Olivar does not think the findings in this report are conceptual or theoretical but gives the industry a practical data set to operate with. “One of the calls for action that we want to ask the industry after the report is launched and validated is to try different mechanisms to see what it will look like if we redistribute value because there is enough value,” she said.

“The problem we have is that there are no mechanisms to trickle that value down.”

“Two key interventions are needed; sector commitments on sourcing practices that enable value redistribution, and supply chain partnerships that design and implement mechanisms for adding, creating, and transferring value,” said Tessa Meulensteen, director of agri-commodities with the IDH. “With the right mechanisms, companies can more easily comply with due diligence and reporting requirements, and ensure a sustainable supply of coffee in the long run.”

It’s clear that coffee growing is economically not viable for farmers. The fact that there is value in the sector is both a chilling alarm that industry patterns need to be changed and a hopeful beacon that there’s a pathway to building a sustainable industry. This report will hopefully serve as a template for future studies and a call to action for downstream agents to begin rethinking how they can actively redistribute value.